Many investors talking about the next global financial crisis after 2008.

They say there is a circle like 1997 Asian Financial Crisis, 2000 dot.com bubble, 2008 Global Financial Crisis and now comes to 2018...

Everybody is talking about the crisis but no one knows when the crisis will happen.

In fact, financial crisis is happening every year.

You can simply google on List of economic crises then all the history will be listed down for you.

The question is, how can you turn the crisis to opportunity?

Are you ever ready on the next crisis?

Now, you go back to study your own portfolio...

100% cash (FD)?

100% equities (stocks)?

100% properties?

100% unit trust funds?

100% on own business?

Non of the above?

If you are holding some unit trust funds in your portfolio, what would you do with it?

Stay put? Re-balancing your portfolio? Or keep investing?

There is always no 100% right answer in investment.

I would say portfolio management plays an important part in this situation.

(depend on case to case, different investor may has different planning on the same situation)

Here is an example for an investor who has invest in unit trust for more than 10 years and the portfolio is making profit more than 7% p.a.

By concerning about the next c\major crisis is coming in the near future (it could be not happen)

The investor may consider to shift / change the unit trust portfolio to 4-5-1 formation.

(refer the picture below)

I always like to refer the unit trust investment to a football match. You need to change your formation during the game depend on situation changed. The person who in charge the team on the tactic and strategy is always the team coach or manager, who is actually the UTC / financial planner.

Of course the team owner is the investor, who has the 100% right to make any decision on the investment. There is no right or wrong in investment process, the key is communication in between the investor and UTC (team owner and the team coach)

By the 4-5-1 formation, it may looks like a defensive pattern but in fact this format can switch to attacking when there is an opportunity arrive.

By the 4-5-1 formation, it may looks like a defensive pattern but in fact this format can switch to attacking when there is an opportunity arrive.The 4 defenders with the goal keeper are playing in the defending role (Balanced Funds) and the 2 Defensive Midfielder and 2 Wing players in the defending role as well (Mixed Asset Funds). The number 10 player who is playing in the Attacking Midfield can attack any time when the opportunity arrive, where the only in front Forward will wait for opportunity (Local Equity Funds)

Look at the football team formation picture again, you will notice that there are substitute players on the bench. They are actually representing your backup / extra money to top up more when you see the opportunity. Example, player might get injured during the game and you need to sub them by the reserve players.

Look at the football team formation picture again, you will notice that there are substitute players on the bench. They are actually representing your backup / extra money to top up more when you see the opportunity. Example, player might get injured during the game and you need to sub them by the reserve players.The process could be look like the diagram below :

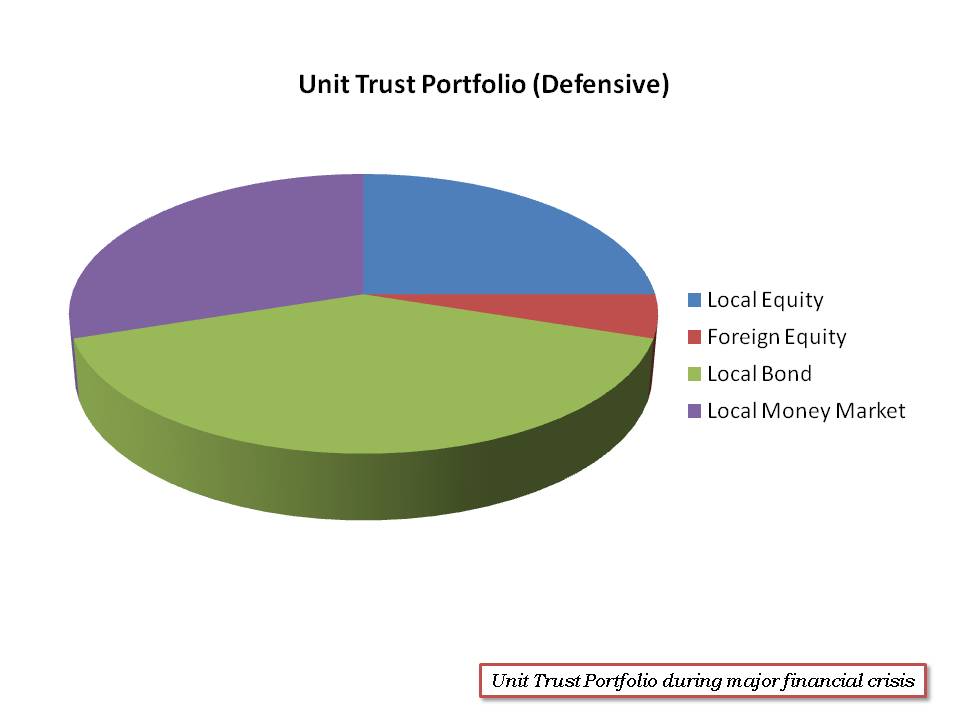

Before the major financial crisis to market panic, market over sold, bad news around every corner, lack of confident to market not moving. The process could take 3 months to 2 years. During this period, you have to communicate to your UTC/financial planner who is the team coach in the football team. Discuss about your investment strategy, plan and portfolio in your unit trust funds.

If you feel that your previous and existing returns / profits are reaching your target, you may start to change your portfolio into defensive formation.

If you feel that your previous and existing returns / profits are reaching your target, you may start to change your portfolio into defensive formation.Holding more portion into Bond or Money Market in unit trust meaning you are holding more cash.

This format may help you to defend your portfolio when the major crisis arrived, means the whole world is on panic selling. (You have to do this before the crisis happen) Is simple but not easy. No one will know the exact timing of crisis.

After the emotional factor, panic feeling had gone from the market. The experts will start to comment their view on the paper. Remember, their job is to write something according to the market. You can use this as your guideline or indicator to make your decision. Do not fall into the emotion after read their comment. Start to shift your unit trust portfolio in the a little bit more aggressive. No more Money Market on hand, more local equity.

Now, few months after the panic and stressful emotion, it could be 6 months or more. Is the time for you to slowly switch your unit trust portfolio into more aggressive formation. In football, you can call it 4-3-3 or 4-4-2 / 2-4-4 formation.

Now, few months after the panic and stressful emotion, it could be 6 months or more. Is the time for you to slowly switch your unit trust portfolio into more aggressive formation. In football, you can call it 4-3-3 or 4-4-2 / 2-4-4 formation.This is the time you should become greed when everybody still in the fear emotion.

Why? Because you are buying at the low unit price for long term (next 5 years)

The above example is NOT suit to all investors in all situations.

There is no 100% perfect plan in investment.

You have to always communicate with your UTC / financial planner from time to time, get his updates and advice. An experience UTC / financial planner should understand your situation and background, your investment objective and your risk profile.

Refer back to List of economic crises... How many time actually you can predict the crisis?

You only can control your portfolio. You only can make decision to lock out profit. You only can change your investment plan according to your situation.

You cannot time the market, that is the reason you invest in unit trust and not directly to the market such as stock/ share investment, currency or commodities.

The key words in unit trust investment is holding power and diversification. Always diversify your investment into different class of assets, region/ countries, industry and sometime UTC.

The key words in unit trust investment is holding power and diversification. Always diversify your investment into different class of assets, region/ countries, industry and sometime UTC.Unit Trust, You Need Trust.

Disclaimer : The contents of this article is based on an experience shared by an UTC. It does not constitute recommendation to buy or sell unit trust funds.

Investors are advised to go back to individual UTC or mutual fund company to get more information about the risk & return on the unit trust funds.

Comments

Post a Comment